Insights

Category:

Let’s talk about two buzzwords in the fintech space– Open Banking and Open Finance. To understand the scale and relevance of these words, we gathered some stats.

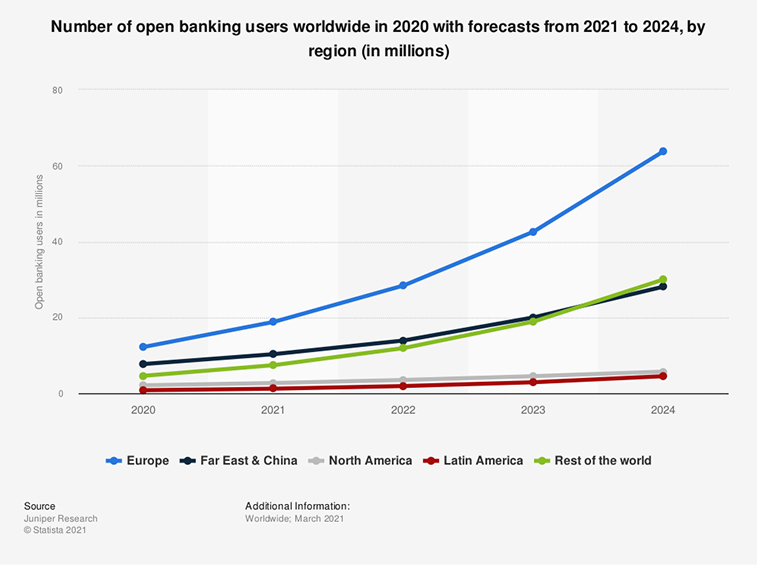

A survey by Statista showed that the number of open banking users worldwide is expected to grow at an average annual rate of nearly 50 percent between 2020 and 2024. And as of 2020, 24.7 million individuals worldwide used open banking services, a number that is forecast to reach 132.2 million by 2024.

Additionally, McKinsey did a study early this year with 259 open-banking licensed providers and open-banking innovations in the UK. The results showed that two-thirds of these innovations are products or services created by fintech companies or non-bank players and the remaining one-third were innovations offered by banks or building societies.

When we researched further about banks adopting APIs, we saw that there was a growth of nearly 19% between Q4 of 2019 and Q1 of 2020, according to Nordic APIs, and the Asia Pacific region saw the greatest ratio of API products to API banking platforms.

Open banking is a practice that gives open access of financial information and data to third party financial service providers through Application Program Interfaces or APIs. The biggest advantage of open banking is that it moves away from the traditional centralized model and allows consumers, financial institutions, and third-party services providers to create a secure institutional network to access account information and financial data.

Open banking is a practice that gives open access of financial information and data to third party financial service providers through Application Program Interfaces or APIs. The biggest advantage of open banking is that it moves away from the traditional centralized model and allows consumers, financial institutions, and third-party services providers to create a secure institutional network to access account information and financial data.

To explain further, open banking allows regulated websites and apps to access transaction data from bank accounts and payment services so that you can ‘move, manage and make the most of your money’. For lenders, this means more visibility into a consumer’s financial standing. Borrowers, in turn, can have a better understanding of their own finances before taking a loan.

Open Finance is the next step in the Open Banking journey. Financial data such as mortgages, savings, pensions, insurance and consumer credit – basically your entire financial footprint – could be opened up to trusted third party APIs if you give the access.

Open Finance is the next step in the Open Banking journey. Financial data such as mortgages, savings, pensions, insurance and consumer credit – basically your entire financial footprint – could be opened up to trusted third party APIs if you give the access.

So, open finance is basically expanding the open banking concept to more sources of data.

By sharing financial data with trusted third parties, customers could get better deals through tailored value-added products and services. It also gives better visibility and greater control over their data.

The end goal for Open Finance is improved financial health driven by market innovation and competition. The access to information is more secure and more real time for better decision making.

Open Banking is paving the way to the future of fintech and here is a summary of the benefits:

By not adopting open banking, financial institutions are putting themselves at a risk from a regulatory standpoint added to the risk of not meeting customers’ expectations and adapting to latest market trends.

By not adopting open banking, financial institutions are putting themselves at a risk from a regulatory standpoint added to the risk of not meeting customers’ expectations and adapting to latest market trends.

We work on automation solutions leveraging Open Banking, for a lot of banks and financial institutions across the US and we see that Open Banking is the way forward.

At Lateetud, we make automation Intelligent. And Intelligent Automation has a large role to play in open banking digital transformation. To know how, talk to us at www.lateetud.com.

Grishma Valliyod December 17, 2021